2026 Mid-Year Market Outlook: 10 Charts On Market Highs And Key Client Topics

The first half of 2026 has seen headline-driven market volatility, from geopolitical events to inflation risks. Given the level of volatility, many investors may have assumed that equity markets would be lower in the middle of the year. However, the S&P 500 posted positive returns (hitting several all-time highs earlier in the year) amid continued strong corporate earnings, rewarding those who managed to watch the headlines and invest.

In this articleClearnomics CEO James Liu explores how advisors can frame news headlines for clients in a data-driven way, ensuring they maintain perspective and understand that periods of uncertainty don’t lead to poor equity market returns.

Looking at equity markets, the energy sector took a hit in the first half of the year amid rising oil prices linked to the conflict with Iran, although some tech stocks were supported, as well as enthusiasm around artificial intelligence (AI) developments. Global stocks also joined the US market in showing positive results in the first half of the year, with both developed and emerging markets posting gains. At the same time, valuations (as measured by the S&P 500’s forward price-to-earnings ratio or Shiller’s cyclically adjusted price-to-earnings (CAPE) ratio) remain historically high (although these data points cannot predict where the market is headed next).

Inflation has picked up this year, with the Consumer Price Index (CPI) rising 4.2% year-on-year in May, a multi-year high. However, the figure was largely driven by the energy sub-component, which jumped 23.5% year-on-year, while the core CPI (which excludes food and energy) rose just 2.9% over the same period – suggesting that the core inflation figure may moderate if the decline in oil prices over the past few weeks continues.

Inflation plays a major role in the minds of decision makers at the Federal Reserve (alongside this year’s tightening labor market), in addition to affecting the prices consumers pay. In the year After starting a rate cut at the end of 2024, expectations for further cuts earlier this year have shifted, with investors now anticipating rate hikes in the coming months. The Federal Open Market Committee appears to be split, with roughly half of members expecting rates to remain unchanged through the end of the year and half expecting them to rise.

Although future federal interest rate decisions remain to be seen, current interest rates are elevated across the entire US Treasury yield curve. While bond yields have been relatively subdued so far this year, current yields could help return fixed income to its traditional role as a portfolio stabilizer and income generator. On the other side of the coin, higher bond yields can act as a headwind for equity prices, as they increase the attractiveness of bonds as an alternative and increase the discount rate applied to future earnings.

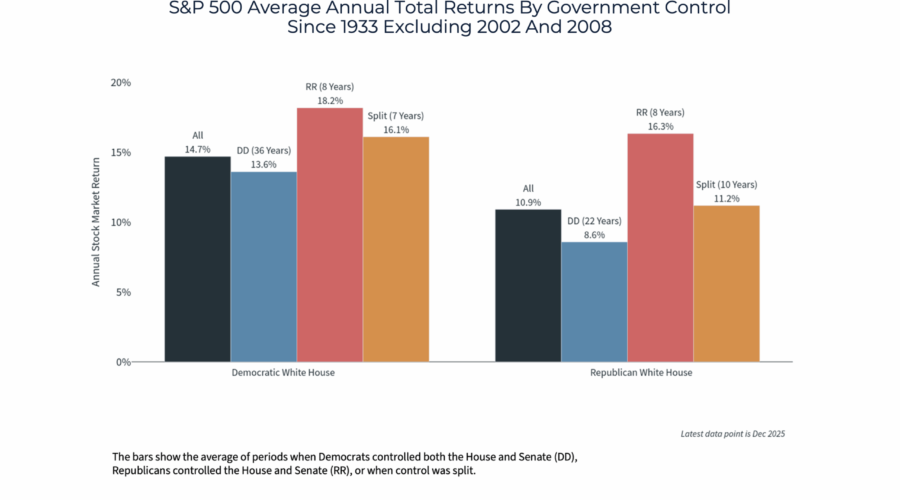

Ultimately, the bottom line is that while headlines can drive short-term market movements, fundamentals like corporate earnings drive long-term returns. This suggests that financial advisors have an important role to play in providing clients with a broader market view and showing them how their asset allocation is designed to meet their short- and long-term goals!