Private Fund Due Diligence: A Checklist For Reviewing Governing Documents And Operational Controls

For most of our history, the financial advisory domain has been helping clients achieve their retirement and other savings goals by investing their savings in publicly traded stocks and bonds that provide the opportunity for long-term growth. While some of the vehicles have changed over time—from individual securities, to mutual funds, to exchange-traded funds—the basic continuity is that all these issuers are registered and subject to Securities and Exchange Commission (SEC) reporting standards that require detailed and extensive disclosure about the issuer, the business, and the securities offered. More recently, as companies stay private longer and issue more private equity and debt, private investments and funds have become more prevalent, and more advisory firms are now exploring whether or not to include private funds in client portfolios. However, due to the strict disclosures required from issuers due to SEC registration and reporting, it is more difficult for advisors to conduct due diligence on private funds, which have investment and legal risks that are not typical of most government investments.

In this guest postRich Chen, founder of Brightstar Law Group, explores the practical precautions advisors should take when considering a private fund investment, focusing specifically on what to look for in governing documents and the private fund’s operating system.

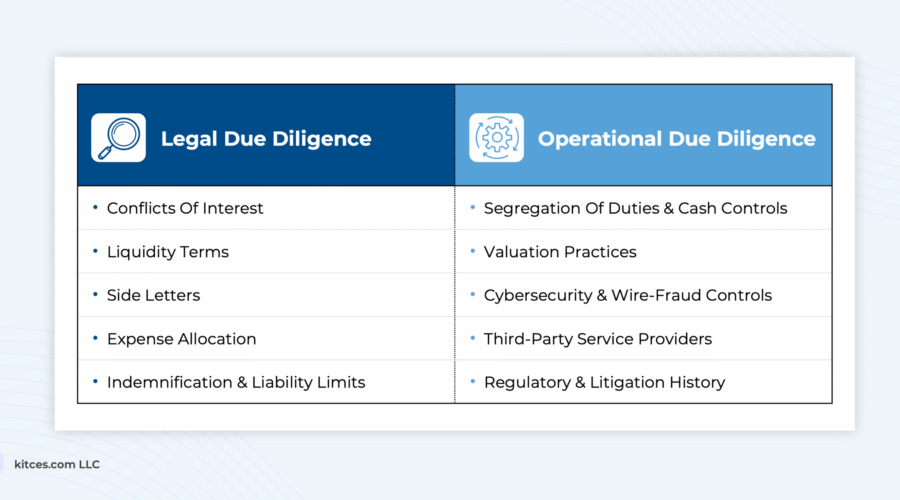

The starting point in due diligence is to realize that what is stated in the legal documents may differ significantly from the marketing materials of a private fund, because the latter is intended to attract investors. to the By focusing the fund on opportunities, the foregoing is written to minimize the risks to the fund’s sponsor (thus clearly indicating the rights of investors putting dollars into the fund). Accordingly, a detailed review of the governing documents will reveal conflicts of interest (for example, between the fund’s sponsor and affiliates), limitations on the investor’s ability to withdraw from the fund’s investment (which can often be significant), identify red flags regarding compensation provisions, and detail how expenses are allocated between investors and fund management. In addition, proper monitoring of the governing documents provides an opportunity to inquire about “side letters” that other investors may have preferred or have special rights or return opportunities.

Beyond due diligence on legal documents, it’s important to evaluate how well private funds operate and how effective they are at protecting investors. For example, does the private fund identify key functions, ensure dual authorizations for payments, use an external custodian or separate accounting firm, and conduct annual audits? These measures can greatly reduce the risk of fraud or misuse by the administrator or employees. Likewise, advisors can ask about the firm’s cybersecurity and client data protections, conduct background checks on the fund sponsor’s history (to check for prior legal issues or enforcement actions!), and determine how the firm will value its assets (and typically charge interest or other management fees based on those valuations).

Finally, Chen offers a due diligence checklist to help support the process, although specifically completing the checklist ‘mechanically’ is not sufficient. Instead, the SEC expects to demonstrate that advisors are thoughtful in their inquiries and review the answers provided, while demonstrating timely documentation, to demonstrate the robustness of the process—for which advisors may seek to engage outside providers in due diligence (especially if their internal resources are limited). The growth of companies in the private market represents a great opportunity for clients to invest, but those who are used to the natural protection that the SEC has built in the public markets should be aware that there are special risks in private equity and loan funds, which require at least a sufficiently careful due diligence process from financial advisors (the SEC will take enforcement actions against additional measures only marketing materials and representatives of private fund sponsors).