Withholding Taxes on Dividends in Europe

In June 2026, the European Commission recommended a Tax Omnibus Package to facilitate the EU direct taxesTaxes are levied directly on individuals and organizations and are not expected to be passed on to a single payer (unlike indirect taxes such as sales taxes and duties), although the economic burden may still fall on some. Often with indirect taxes, such as personal income taxes, the tax rate increases as the taxpayer’s power, or financial resources, increases, creating what is called ap. schedule. Among other things, it will remove the quota requirement to exclude dividends, profits, and royalties between EU companies from holdingWithholding is income that an employer takes out of an employee’s wages and remits to federal, state, and/or local government. It is calculated based on the amount of income, tax payer status, amount of allowances requested, and any additional amount requested by the employer. taxTaxes are mandatory payments or charges that local, state, and national governments collect from individuals or businesses to pay for general government services, goods, and services.. Payments that leave the EU without paying tax in the receiving state will instead be subject to cross-border tax. This step will reduce the main source two taxesDouble taxation is when taxes are paid twice on the same dollar of income, regardless of corporate or individual income. and administrative complications for cross-border investment in Europe.

How to Save Foreign Taxes – Keep a Job?

Withholding tax is a tax that requires companies that pay dividends, interest, and royalties to foreign investors or businessmen to withhold a certain amount to the tax authority in the country of origin.

Consolidated taxation applies to income in its source jurisdiction, rather than in the recipient’s home jurisdiction, where taxes are usually paid. This can help to ensure that resident taxpayers comply with tax regulations and do not evade taxes through this method transfer income to other jurisdictions. However, tax avoidance can lead to double taxation and cross-border diversion of income when paying the income of domestic and foreign investors.

In practice, investors can pay the withholding tax paid abroad on the domestic tax due in their country, but not always to the full amount or without delay. Therefore, even the cooperative system can create a double tax and administrative burden, especially when the repayment or credit procedures are delayed, inconsistent, or limited by the limits of the agreement.

For example, when a company joins Germany pays €100 in dividends to the investor in it Greece, Germany retained €26.37 (including a 5.5 percent bond). extra chargeA surtax is an additional tax levied on top of an existing business or personal tax and may have a broad or progressive structure. Additional taxes are implemented to fund a specific program or initiative, while revenue from a general tax source, such as personal income tax, usually covers a wide range of programs and activities. imposed on the prohibited amount) under local law. Under the second tax treaty which limits the tax to 25 percent, the investor can receive a bond fee of €1.37 from the German tax authority. Greece generally taxes the surplus of residents’ income at a rate of 5 percent. But, when it was received from abroad, Greece paid foreign taxes of the amount already withheld in Germany, up to the amount of local taxes. Due to financial differences, a Greek resident pays a tax of 25% on the profit he receives from a German company, instead of 5% if it is received from a company in Greece or another region without tax on profits, such as United Kingdom.

When withholding taxes result in double taxation or high administrative burdens, they may prompt investors to invest in assets with lower pre-tax returns or hold real estate to avoid these burdens.

Closing the Gap in the Investment Sector

Ideally, policy makers should aim to guarantee the free movement of capital across borders by eliminating double taxation and internal and external payment conflicts to allow investment in assets and areas with the highest returns.

Therefore, double taxation agreements between countries often include provisions to reduce the amount of withholding tax. At the corporate level, EU legislation already prohibits member states from retaining the profits paid by a subsidiary to its parent company in a different member state, if certain conditions are met.

European Commission evaluation that extending the rules to exempt profits, royalties, and payments between EU companies from withholding tax regardless of the percentage of withholding would increase long-term GDP by at least 0.043 percent, at a cost of 0.027 percent in general income. European companies will save about 700 million euros per year in payment costs and another 700 million euros in the opportunity to spend at the moment to recover the delay, while avoiding two taxes will generate 3.8 billion euros in tax savings.

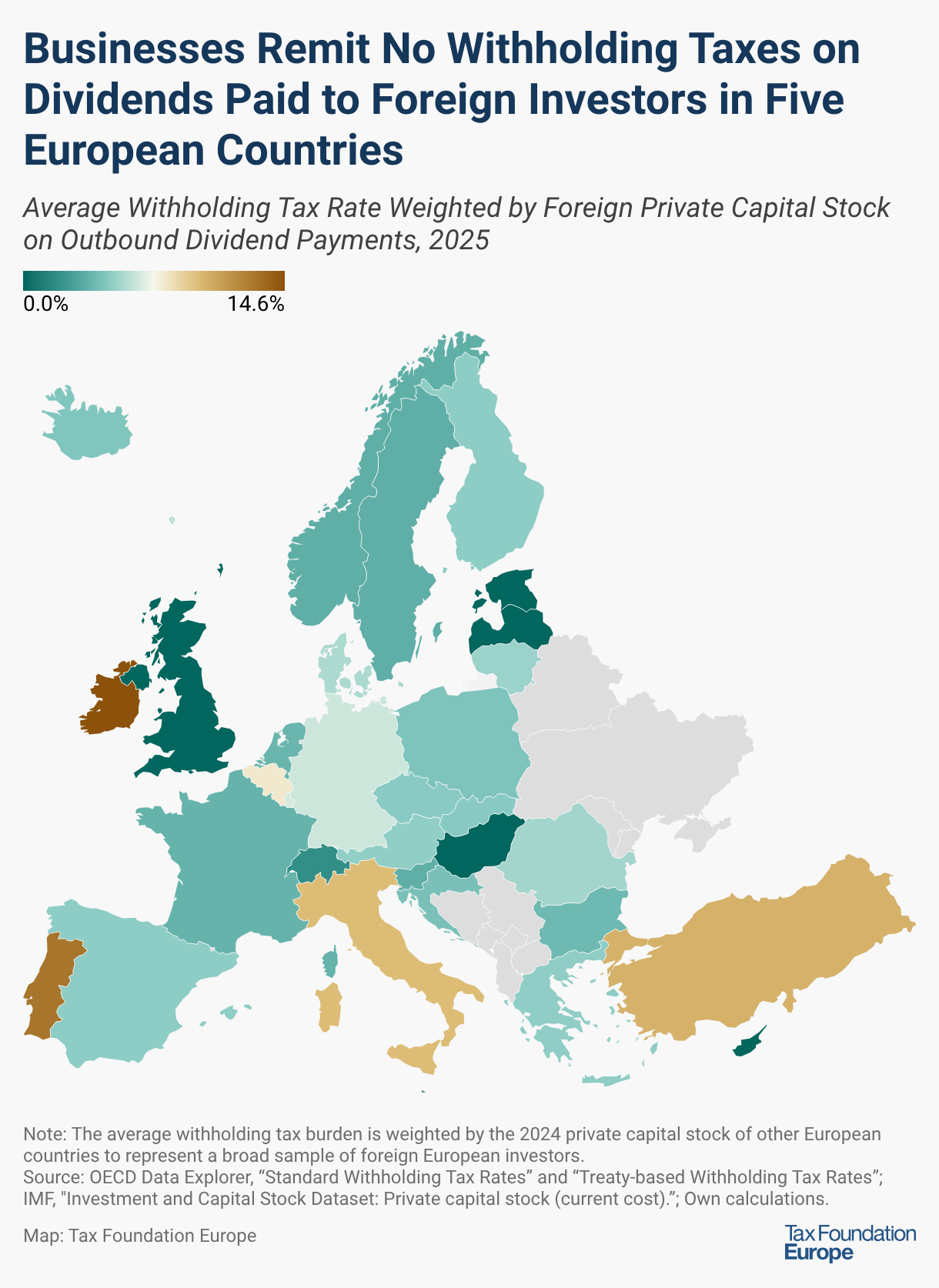

Withholding Tax Burden on Inbound and Outbound Payments in Europe

The maps below show the import and export tax rates for all 32 European OECD and EU countries, which apply when income crosses their borders. The average amount is weighted by the 2024 private equity investments of other European countries for a fixed-income, European portfolio. A country’s foreign exchange rate shows a direct impact on the country’s savings opportunities for investors, while foreign exchange rates reflect the state of trade finance.

For the ease of cross-border savings and investment, policymakers should seek to reduce the risk of double taxation and administrative complications that may be caused by withholding taxes for inward or outward payments.

European countries vary widely in their tax rates, with Belgium, Greece, Italy, Portugal, Same to you Turkey it shows constant weight in both sides and types of payment. In contrast, Hungary, Switzerland, Great Britain, as well Czech Republic they generally provide more favorable conditions for cross-border savings and investment.

On average, savers investing in a large European stock portfolio face an income tax rate of 5.6 percent. Investors residing in Cyprus (15.1 percent), Portugal (11.4 percent), and Greece (11.3 percent), face the highest entry costs on foreign-sourced profits. In contrast, investors in Switzerland (2.3 percent) face the lowest inbound costs on dividends, followed by the United Kingdom (3.1 percent) and Denmark (section 3.4).

For interest payments, investors who receive cross-border interest income face an average withholding tax rate of 3.4 percent. Those living in Cyprus (8.5 percent) face the highest rate of foreign interest, followed by Turkey (7 percent) and Portugal (6.2 percent). In contrast, the Czech Republic (1 percent), Hungary (1.3 percent), and Slovak Republic (1.4 percent) record the lowest cost of entry on profit.

The business that lives in it Ireland (14.6 percent), Greece (14 percent), Portugal (13 percent), and Turkey (10.3 percent) produce the highest export costs paid to foreign investors, while doing business in Cyprus. Estonia, Hungary, Latvia, Malta, and the United Kingdom are not required to pay withholding tax on foreign profits.

Tax protection has been a source of double taxation and administrative complications for cross-border savings and investments in Europe. The introduction of the current exemption for the deduction of withholding tax on intra-EU distributions, profits, and royalties regardless of holdings will directly address this conflict and bring the Single Market closer to the free movement of capital that it was intended to ensure.

Tax makes sense with us in your inbox.

Subscribe to our newsletter for tax insights that cut through the noise—and make sense.

Average Share of Import and Export Taxes in European OECD and EU Countries, 2025

Note: The average tax burden is borne by private equity investments in 2024 of some European countries to represent a large sample of European foreign investors.

Source: OECD Data Explorer, “Tax Income Standard” and “Convention-based Tax Integration Analysis”; IMF, “Investment and Capital Information: Private equity (current prices)”; List of authors.

Share this article